Overviews

Author: Natalia Grishchenko

July 15 2023

(Zero) Growth Instead of Recession: Brief and Short-Term Estimates

One of the current issues on the agenda of most economic debates and assessments is the possibility of a recession in 2023 and in the short term until 2024. What factors, indicators can affect recession risks, what are their dynamics and what are the economic forecasts? This analytics is in our brief review.

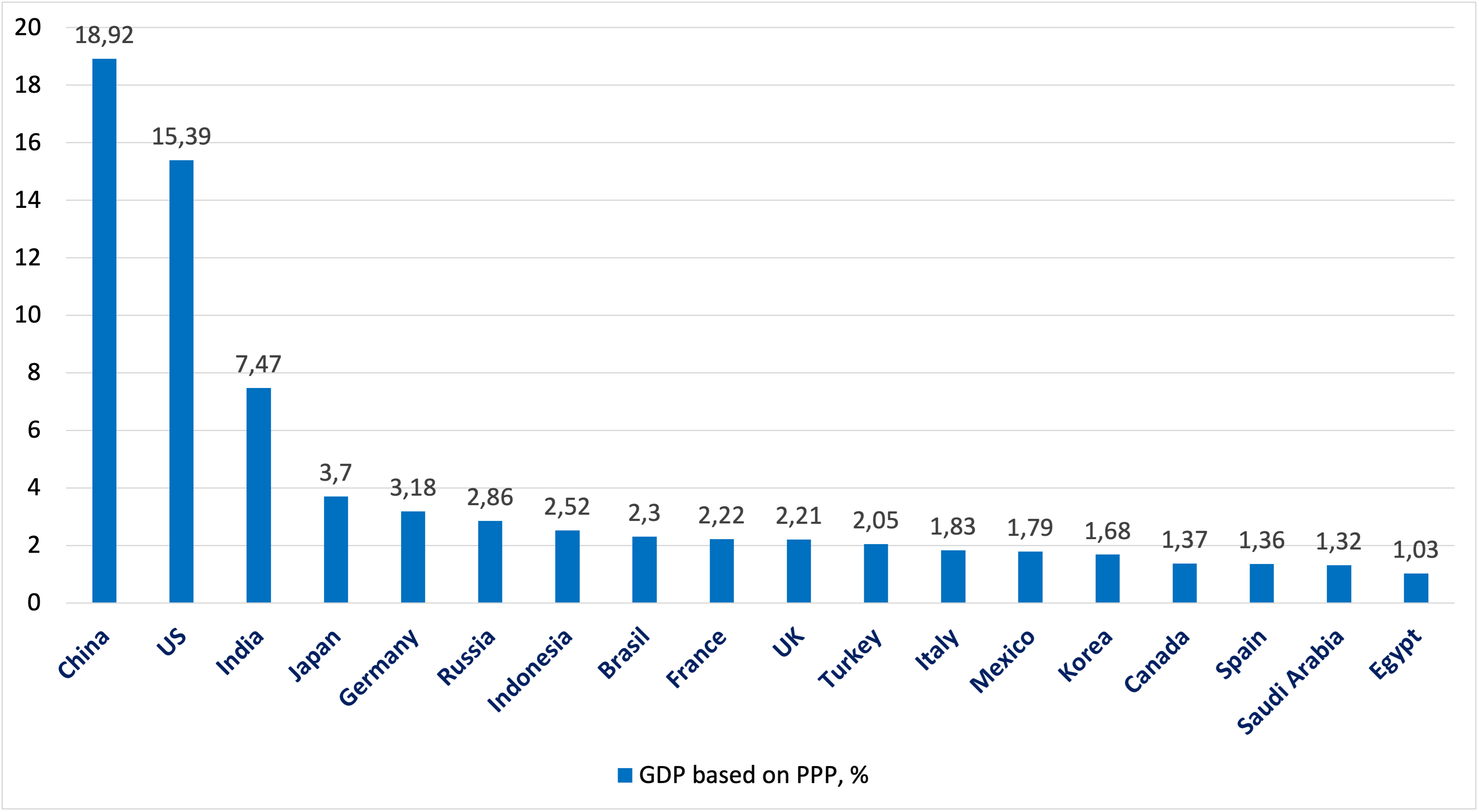

As an example for evaluation, we selected a number of countries, both developed and developing, in terms of their GDP (growth in domestic product) based on PPP (purchasing power parity), which is represented by the International Monetary Fund (IMF): at least 1%. Eligible for this criterion are 18 countries in 2023: China, USA, India, Japan, Germany, Russia, Indonesia, Brazil, France, United Kingdom, Turkey, Italy, Mexico, South Korea, Canada, Spain, Saudi Arabia, Egypt (Fig. 1). Еhere are other relevant indicators that can be used to forecast economic dynamics and the possibility of a recession. For example, models that take into account the value of interest rates, business cycles, household behaviour, and others.

Figure 1. GDP based on PPP, %, 2023 (selected countries, > 1%)

Source: IMF, World Economic Outlook, April 2023

We are evaluating a number of indicators, changes in which potentially indicate the probability of a recession. Here we analyze three of these indicators in a national context: national annual GDP growth, exports of goods and services, and consumption expenditure. We compare these figures in 2022 with 2009, the worst-hit year since the 2008 financial crisis, to measure the difference and potential recession risks. Data used is from the IMF and the World Bank (WB).

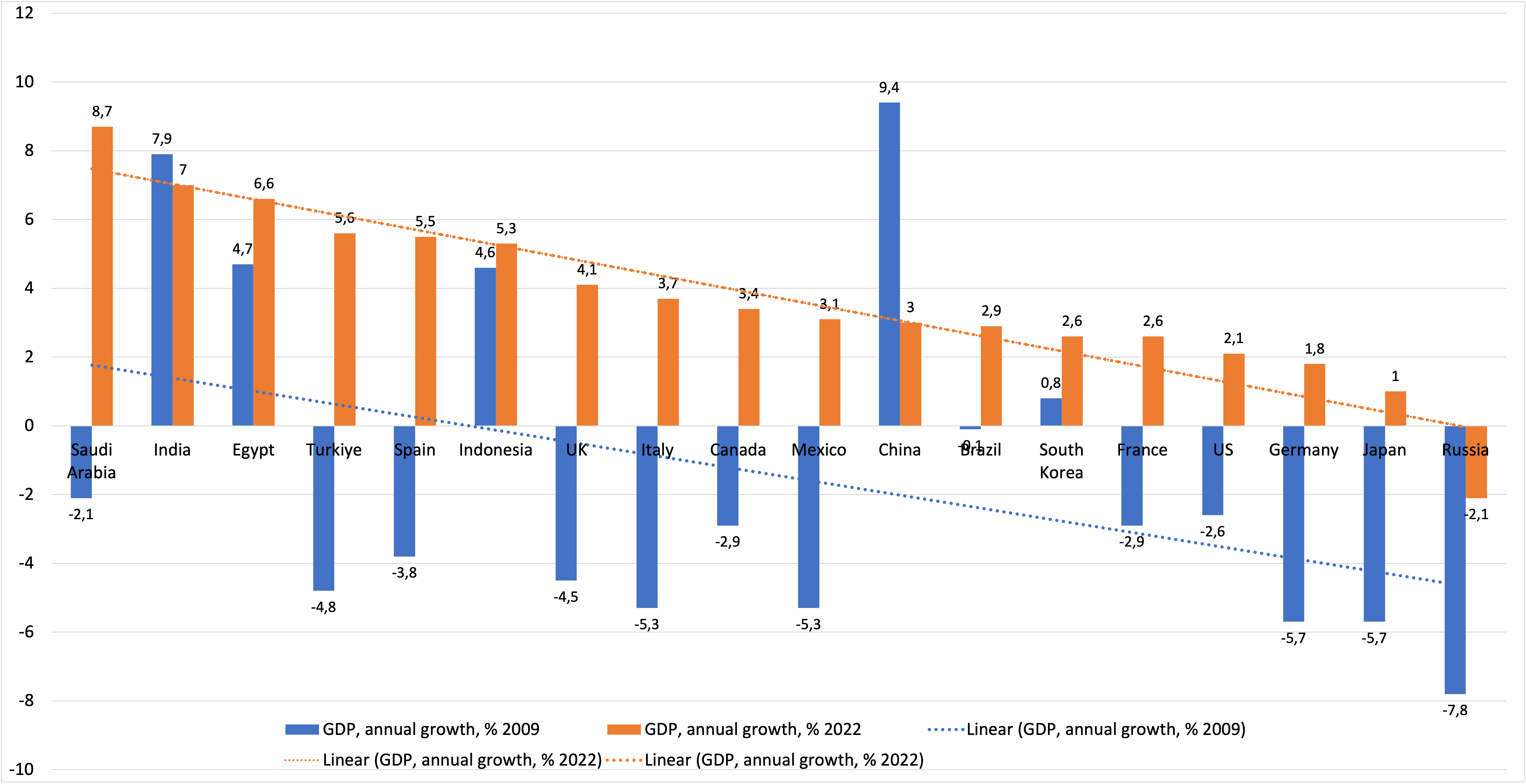

The annual growth of GDP shows that for most countries the situation in 2022 is more stable and relatively prosperous compared to post-crisis 2009 (Fig. 2). Almost all countries had GDP growth in 2022 except for China and India, whose growth in 2009 was higher than in 2022, 9.4% instead of 3% and 7.9% instead of 7%, respectively. This dynamic allows us to say that the world economy, using the example of the observed countries, demonstrates greater resistance to the impact of high inflation, the energy crisis, financial instability, and public debt.

Figure 2. GDP, annual growth, 2009, 2022, %

Source: WB

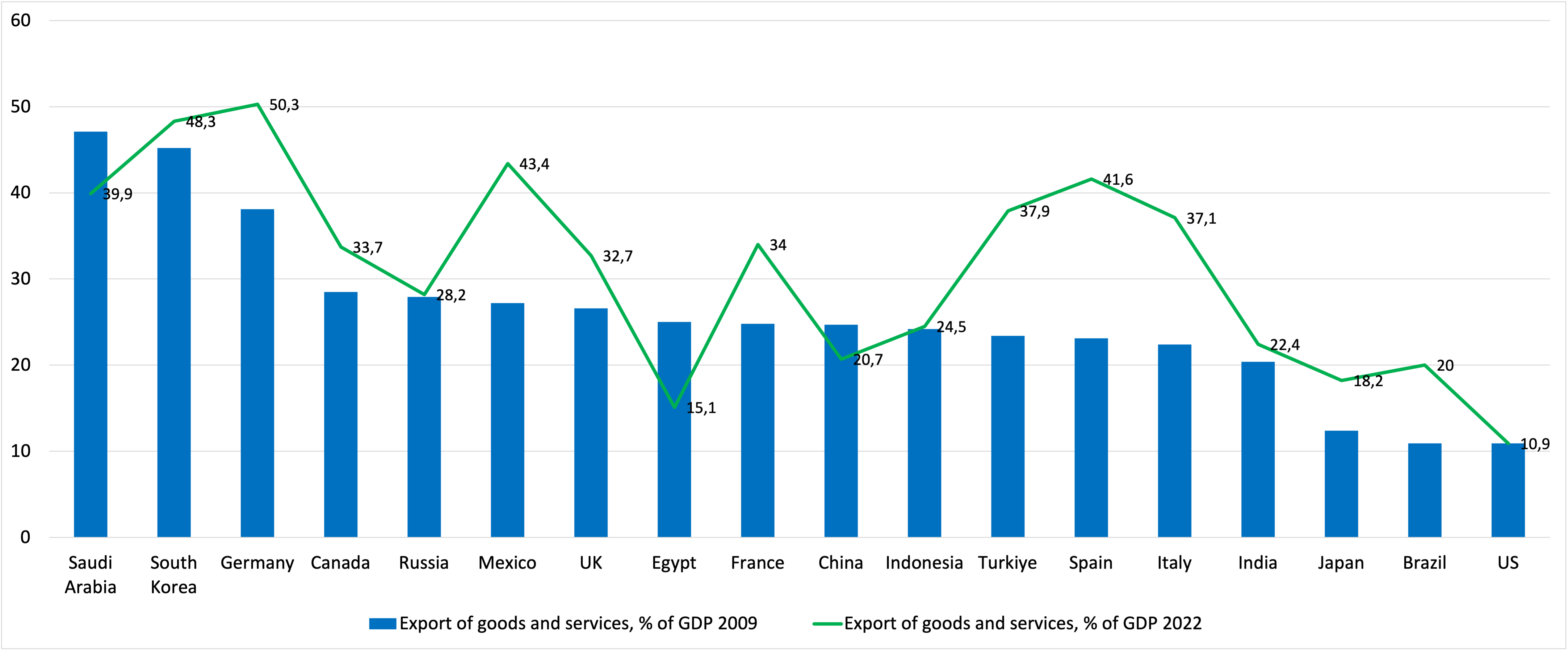

The export indicator also shows better dynamics compared to the crisis year of 2009 (Fig. 3). With the exception of Saudi Arabia, Egypt and China, other countries are showing stronger growth in exports of goods and services in 2022 compared to 2009.

Figure 3. Export of goods and services, % of GDP, 2009, 2022

Source: WB

Note: For US, Japan the data is for 2021.

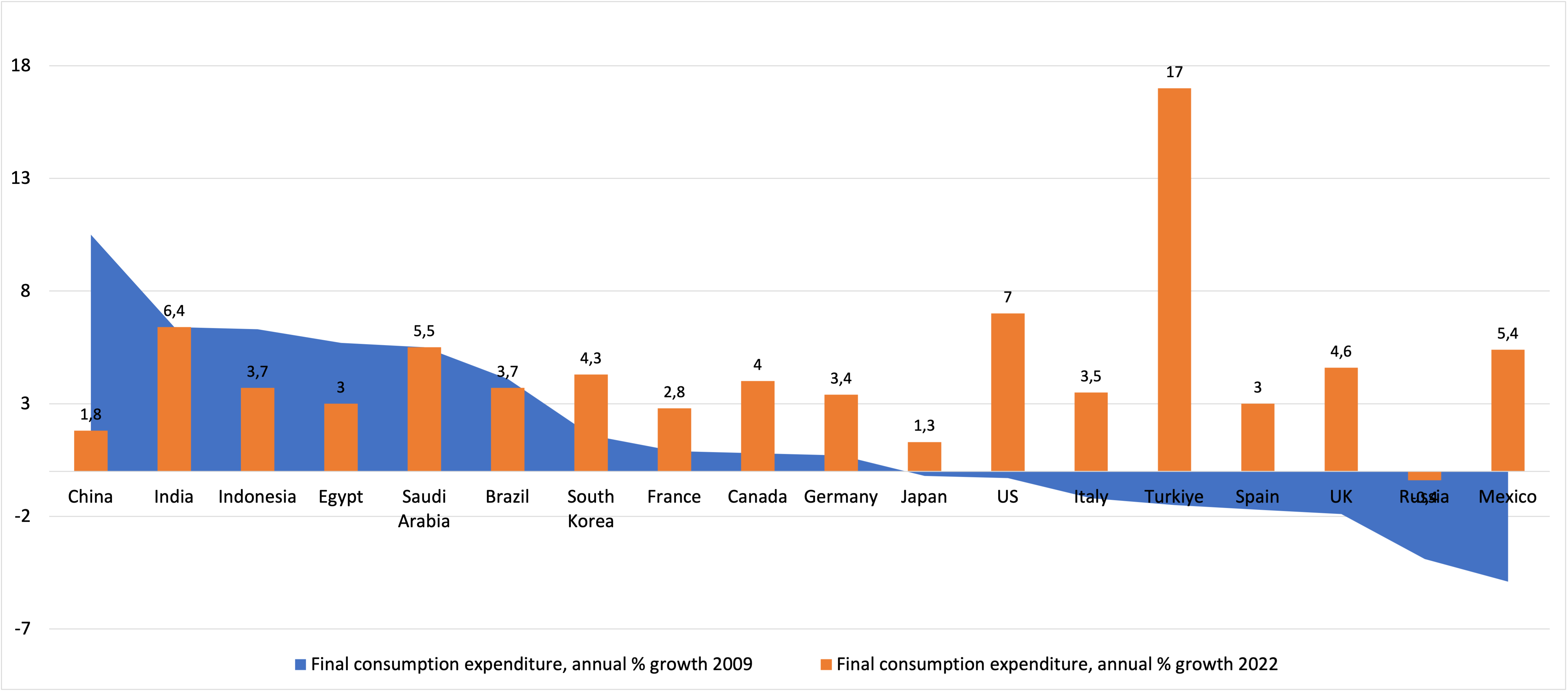

The consumption expenditures show different trends for assessing and forecasting the economic situation in 2022 compared to 2009 (Fig. 4). For most countries in the sample, there is an increase in annual spending on consumption in 2022 compared to 2009. This may indicate greater household confidence and, accordingly, not in the decline in consumption, which manifests itself during a crisis. The exceptions are China, Indonesia and Egypt.

Figure 4. Final consumption expenditure, annual % growth, 2009, 2022

Source: WB

Note: For US, Japan the data is for 2021.

A brief analysis shows a more confident situation in the economy in 2022 and in the short term until 2024 compared to the 2007-2009 crisis. For most of the countries under consideration, the analyzed indicators are in a relatively more stable position between these periods. Based on this, we can assume the absence of a recession in the definition of decline in the short term.

However, other factors should also be taken into account that could influence the current situation and lead not to a recession, but to slower or weak growth in the mid-term. Among the negative factors are high inflation, relatively "expensive" money, which limit investments in the economy and subsequent growth. To this should also be added the impact of the transition to a green economy, technological changes, further (de)globalization.

Based on these brief analytics and reports from IMF, WB, OECD, World Economic Forum, the following conclusions can be assumed:

- the economic indicators reviewed here and others show a certain level of confidence and stability in the global economy recovering from the Covid-19 pandemic,

- low or close to zero growth may be the most obvious economic development scenario,

- due to the significant differences across countries that we noted, the direct effects will be at the national level, since countries have their own strong (weak) economic indicators. For example, such strong indicators may include low inflation in China, a strong job market in the US, or a moderate interest rate in Europe,

- short- and mid-term situations regarding economic development are influenced by the above and other factors, as well as under weakly predictable force majeure circumstances such as a pandemic, a local financial crisis or others.

Despite the positive assessment of avoiding a recession instead of a slight increase, it would be practical to prepare for possible situations and take into account the conditions for doing business, home economics and personal finance: reducing operating costs and debt, diversifying sources of income and investments, contributing to personal capital in the form of health, education and personal development.

Citation:

Grishchenko Natalia. (Zero) Growth Instead of Recession: Brief and Short-Term Estimates. https://accorde.pl, 2023.07.15.